We are here to help, contact us today:

Phone: 02 6766 4288

Web: www.lockharts.au

Email: admin@lockharts.au

The Fringe Benefits Tax year (FBT) ends on 31 March. We explore the problem areas likely to attract the ATO's attention.

In late 2022, the Government introduced a concession that enables employers to provide some electric vehicles to employees without incurring the 47% fringe benefits tax (FBT) on private use.

The exemption applies to the use of electric cars, hydrogen fuel cell electric cars or plug-in hybrid electric cars if:

If your business is planning on acquiring an electric vehicle, be aware that from 31 March 2025, the FBT exemption will no longer apply to plug-in hybrid electric vehicles unless the vehicle met the conditions for the exemption before this date and there is already a binding agreement to continue to use the vehicle privately after this date.

The problem areas

The exemption only applies to employees - For the FBT exemption to apply, the vehicle needs to be supplied by the employer to an employee (including under a salary sacrifice agreement). Partners of a partnership and sole traders are not employees and cannot access the exemption personally.

If LCT applies to the car it will never qualify for the FBT exemption. For example, if the EV failed the eligibility criteria in 2022-23 when it was first purchased because it was above the luxury car limit of $84,916, the fact that it resold in 2023-24 for $50,000 does not make it eligible for the exemption on resale. Likewise, if the car was used by anyone (including a previous owner) before 1 July 2022 then it will probably never qualify for the FBT exemption.

Home charging stations are not included in the exemption. The FBT exemption includes associated benefits such as registration, insurance, repairs or maintenance, but it does not include a charging station at the employee’s home. If the employer instals a home charging station at the employee’s home or pays for the cost, then this is a separate fringe benefit.

FBT might not apply but you do the paperwork as if it did. While the FBT exemption on EVs applies to employers, the value of the fringe benefit is still taken into account when working out the reportable fringe benefits of the employee. That is, the value of the benefit is reported on the employee’s income statement. While you don’t pay income tax on reportable fringe benefits, it is used to determine your adjusted taxable income for a range of areas such as the Medicare levy surcharge, private health insurance rebate, employee share scheme reduction, and certain social security payments.

What about the cost of electricity? The ATO’s short-cut method can potentially be applied to calculate reportable fringe benefit amounts and applies a rate of 4.20 cents per kilometre. If you are not using the short-cut method, you need to have a viable method of isolating and calculating the electricity consumption of the car.

The exemption does not apply if the employee directly purchases or leases the EV. If an employee purchases or leases the EV directly, and the employer reimburses them under a salary sacrifice arrangement, the FBT exemption does not apply because this is not a car fringe benefit. However, the exemption can potentially apply to novated lease arrangements if they are structured carefully.

Not all electric vehicles are cars. To qualify for the exemption, the EV needs to be a car – electric bikes and scooters do not count, nor do vehicles designed to carry a load of 1 tonne or more or that carry 9 passengers or more.

Not registering. If you have employees, it is unusual not to provide at least some fringe benefits. If your business is not registered for FBT but you have provided entertainment, salary sacrifice arrangements, forgiven debts, paid for or reimbursed private expenses, or have provided accommodation or living away from home allowances, it’s important that the FBT position is reviewed carefully. The ATO targets businesses that aren’t registered for FBT.

When employees travel. There has been a renewed focus recently on whether employees are travelling in the course of performing their work (deductible and not subject to FBT) or travelling from home to their place of work (not deductible and subject to FBT). The Federal Court decision in the Bechtel Australia case is a good example. The case dealt with the travel of fly-in-fly-out workers between home and their worksite - involving flights, ferry and bus travel. The Court found that the employees were travelling before they commenced their shift and that the employer was liable for FBT in connection with the transport that was provided. The case highlights the need for employers to ensure that they are fully aware of the connection between work and travel.

Late last year, thousands of taxpayers and their agents were advised by the Australian Taxation Office (ATO) that they had an outstanding historical tax debt. The only problem was, many had no idea that the tax debt existed.

The ATO can only release a taxpayer from a tax debt in limited situations (e.g., where payment would result in serious hardship). However, sometimes the ATO will decide not to pursue a debt because it isn’t economical to do so. In these cases, the debt is placed “on hold”, but it isn’t extinguished and can be re-raised on the taxpayer’s account at a future time. For example, these debts are often offset against refunds that the taxpayer might be entitled to. However, during COVID, the ATO stopped offsetting debts and these amounts were not deducted.

In 2023, the Australian National Audit Office advised the ATO that excluding debt from being offset was inconsistent with the law, regardless of when the debt arose. And by this stage, the ATO’s collectible debt had increased by 89% over the four years to 30 June 2023.

The response by the ATO was to contact thousands of taxpayers and their agents advising of historical debts that were “on hold” and advising that the debt would be offset against any future refunds. These historical debts were often across many years, some prior to 2017, and ranged from a few cents to thousands of dollars. For many, the notification from the ATO was the first inkling they had of the debt, because debts on hold are not shown in account balances as they have been made “inactive”. In other words, taxpayers were accruing debt but did not know as the debts were effectively invisible because they were noted as “inactive.”

In a recent statement, the ATO said: “The ATO has paused all action in relation to debts placed on hold prior to 2017 whilst we review and develop a pragmatic and sensible way forward that takes into account concerns raised by the community.

It was never our intention to cause frustration or concern. It’s important to us that taxpayers have trust in our tax system and our records.”

For any taxpayer with a debt on hold, it is important to remember that just because the ATO might not be actively pursuing recovery of the debt, this doesn’t mean that it has been extinguished.

Out of the $50bn in collectible debt owing to the ATO, two thirds is owed by small business. As of July 2023, the ATO moved back to its “business as usual” debt collection practices. For entities with debts above $100,000 that have not entered into debt repayment terms with the ATO, the debt will be disclosed to credit reporting agencies.

If your business has an outstanding tax debt, it is important to engage with the ATO about this debt. Hoping the problem just goes away will normally make things worse.

From 1 July 2024, the amount you can contribute to super will increase. We show you how to take advantage of the change.

The amount you can contribute to superannuation will increase on 1 July 2024 from $27,500 to $30,000 for concessional super contributions and from $110,000 to $120,000 for non-concessional contributions.From 1 July 2024, the amount you can contribute to super will increase. We show you how to take advantage of the change.

The contribution caps are indexed to wages growth based on the prior year December quarter’s average weekly ordinary times earnings (AWOTE). Growth in wages was large enough to trigger the first increase in the contribution caps in 3 years.

Other areas impacted by indexation include:

For those with the disposable income to contribute, superannuation can be very attractive with a 15% tax rate on concessional super contributions and potentially tax-free withdrawals when you retire. For business owners who might have had an exceptional year or sold their business, it's an opportunity to get more into super. However, the timing of contributions will be important to maximise outcomes.

If you know you will have a capital gains tax liability in a particular year, you may be able to use ‘catch up’ contributions to make a larger than usual contribution and use the tax deduction to help offset your capital gain tax bill.

But, this strategy will only work if you meet the eligibility criteria to make catch up contributions and you lodge a Notice of intent to claim or vary a deduction for personal super contributions, with your super fund.

The bring forward rule enables you to bring forward up to 2 years’ worth of future non-concessional contributions into the year you make the contribution – this is assuming your total superannuation balance enables you to make the contribution and you are under age 75.

If you utilise the bring forward rule before 30 June, the maximum that can be contributed is $330,000. However, if you wait to trigger the bring forward until on or after 1 July, then the maximum that can be contributed under this rule is $360,000.

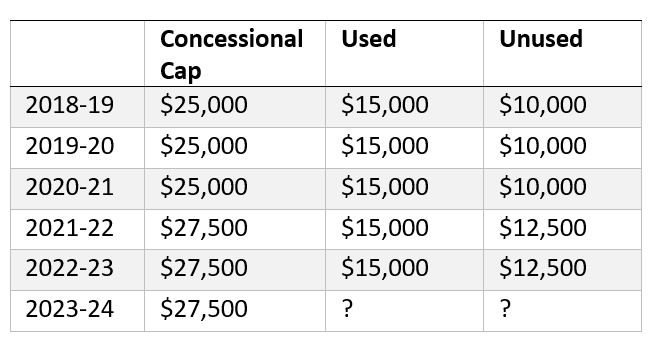

If your super balance is below $500,000 on the prior 30 June, and you want to quickly increase the amount you hold in super, you can utilise any unused concessional super contributions amounts from the last 5 years.

Let’s look at the example of Gary who has only been using $15,000 of his concessional super cap for the last few years. Gary’s super balance at 30 June 2023 was $300,000, so he is well within the limit to make catch up contributions.

Gary could access his $27,500 concessional cap for 2023-24 plus the unused $55,000 from the prior 5 financial years.

If Gary doesn’t access the unused amounts from 2018-19 by 30 June 2024, the $10,000 will no longer be available. Gary could access his $27,500 concessional cap for 2023-24 plus the unused $55,000 from the prior 5 financial years.

The general rate for the transfer balance cap (TBC), that limits how much money you can transfer into a tax-free retirement account, will remain at $1.9 million for 2024-25. The TBC is indexed by the December consumer price index (CPI) each year.

“Life isn't about finding yourself. Life is about creating yourself.”

George Bernard Shaw

The revised stage 3 tax cuts have passed Parliament and will come into effect on 1 July 2024.

Before the new tax rates come into effect, check any salary sacrifice agreements to ensure that they will continue to produce the result you are after.

It’s not uncommon for business owners to pour their money into a business to get it up and running and to sustain it until it can survive on its own. A recent case highlights the dangers of taking money out of a company without carefully considering the tax implications.

A case before the Administrate Appeals Tribunal (AAT) was a loss for a taxpayer who blurred the lines between his private expenses and those of his company.

The taxpayer was a shareholder and director of a private company that operated a business. Over a number of years, he made withdrawals and paid personal private expenses out of the company bank account, but the amounts were not recognised as assessable income.

Following an audit, the ATO assessed the withdrawals and payments as either:

Division 7A contains rules aimed at situations where a private company provides benefits to shareholders or their associates in the form of a loan, payment or by forgiving a debt. If Division 7A is triggered, then the recipient of the benefit is taken to have received a deemed unfranked dividend for tax purposes.

The taxpayer tried to convince the AAT that the withdrawals were repayments of loans originally advanced by him to the company and therefore should not be assessable as ordinary income. Alternatively, he argued that the payments were a loan to him and there was no deemed dividend under Division 7A because the company did not have any "distributable surplus” (a technical concept which limits the deemed dividend under Division 7A).

The AAT found issues with the quality of the taxpayer’s evidence, concluding that he failed to prove that the ATO’s assessment was excessive. This was based on a number of factors, including:

While the taxpayer had tried to explain that some of his loans to the company were sourced originally from borrowings from his brother, the AAT considered this was implausible given the brother’s own tax return showed modest income.

So, how should a contribution from a company owner to get a business up and running be treated? It really depends on the situation, but for small start-ups, the common avenues are:

In making a decision on which is the best approach, it is necessary to consider a range of factors, including commercial issues, the ease of withdrawing funds from the company later and regulatory requirements.

The way you put money into the company also impacts on the options that are available to subsequently withdraw funds from the company. However, the key issue to remember is that if you take funds out of a company then there will probably be some tax implications that need to be carefully managed.

Note: The material and contents provided in this publication are informative in nature only. It is not intended to be advice and you should not act specifically on the basis of this information alone. If expert assistance is required, professional advice should be obtained.

Publication date: 7 March 2024

We are here to help, contact us today:

Phone: 02 6766 4288

Web: www.lockharts.au

Email: admin@lockharts.au